All Services

Our Team

All Services

Teacher Retirement Planning Guidance | BTO Financial Group

Educators often have a retirement puzzle that looks nothing like the private sector. Instead of a single 401(k), teachers may be coordinating simultaneously:

A pension or retirement system

Supplemental plans (often 403(b) and/or 457(b))

Personal savings and spousal income

Social Security rules (which can vary by situation and state)

Healthcare timing and coverage decisions

Teacher Retirement Planning

BTO Financial Group offers education-focused guidance for educators navigating pension benefits and insurance-based retirement planning strategies—designed to help teachers understand their options and plan with confidence.

Why Choose an Education-First Approach?

We emphasize education, clarity, and transparency to help individuals and families better understand insurance-based retirement planning strategies and make informed decisions.

01.

Education Comes First

We prioritize education and understanding, taking the time to explain insurance-based retirement planning options clearly—so you can make decisions that feel informed and comfortable.

02.

Transparent Planning Process

Our approach is built on clarity and transparency. We walk through available options, explain how different strategies work, and answer questions without pressure or obligation.

03.

Professional

Guidance

As a licensed insurance professional, we provide guidance focused on insurance-based retirement planning strategies designed to support long-term planning goals.

Why Teacher Retirement Planning Is Different

Teacher retirement decisions often include:

01.

Vesting rules:

- When Pension Benefits Become Yours.

02.

Service Credit:

- How Years of Service Affect Pension Income.

03.

Retirement Eligibility:

- Age + Service Requirements

04.

Survivor Options:

- Choices That Affect Spouse Benefits

05.

Timing:

- When to Retire and How it Affects Monthly Income

06.

Healthcare:

- Coverage Before Medicare and After

Details vary by retirement system, district, and state—so the goal is to build a clear plan around your specific rules.

Clarity Makes Retirement Planning Simpler

Through an education-first approach, we help individuals and families better understand insurance-based retirement planning strategies and navigate important decisions with clarity. Our focus is on transparency, understanding options, and thoughtful long-term planning.

Clarity Makes Retirement Planning Simpler

Through an education-first approach, we help individuals and families better understand insurance-based retirement planning strategies and navigate important decisions with clarity. Our focus is on transparency, understanding options, and thoughtful long-term planning.

The Teacher Retirement Questions That Matter Most

Education-first planning usually starts with:

- What income do you expect from your pension at different retirement dates?

- Do you want maximum lifetime income, or stronger survivor protection for a spouse?

- What gaps exist between pension income and your desired lifestyle?

- How will healthcare costs fit into the plan?

- Are your beneficiaries current and correctly structured?

How Insurance-Based Strategies Can Support Educators

Mortgage protection is Depending on goals and suitability, insurance-based planning may help with:

01.

Survivor Protection:

A pension may reduce significantly when one spouse passes, depending on the option chosen. Life insurance is sometimes used to help protect a surviving spouse or family members.

02.

Income Structuring:

Some educators explore strategies designed to create supplemental retirement income to pair with pension payments, especially when they want more predictability.

03.

Planning for Timing Gaps

Some teachers retire before Medicare eligibility or before certain benefits begin. Planning can help address these transition years.

04.

Final Expense and Family Protection

With the pension often not enough, many educators want dedicated coverage for final expenses, debt protection, or family needs.

05.

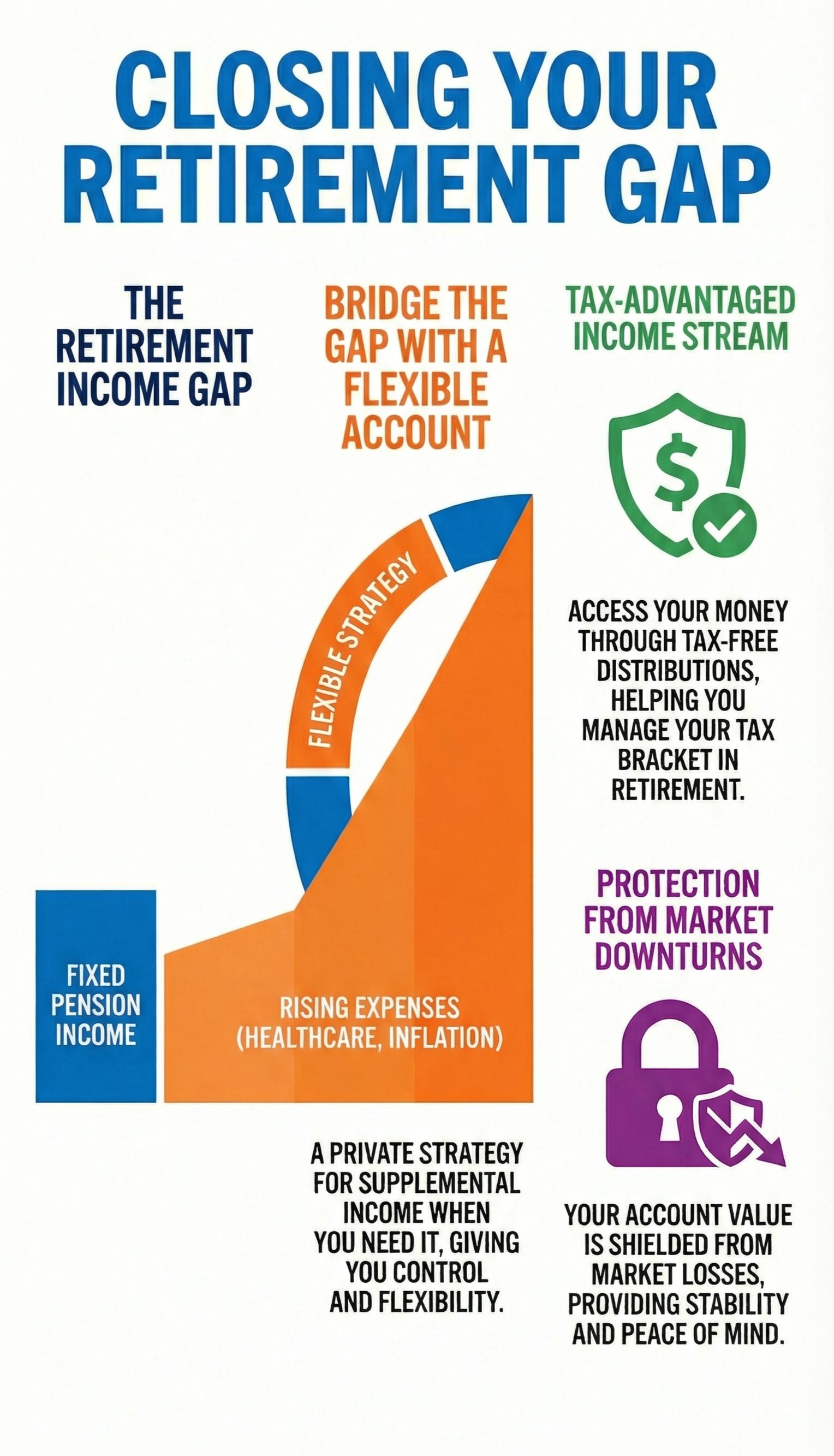

The Retirement Gap

The pension monthly income at retirement often is not enough to meet retirement monthly income required to maintain the lifestyle or even cover basic needs.

06.

Tax Diversification and Flexibilty

Some insurance-based strategies are used to create access to funds that are taxed differently than pension income or required retirement distributions.

The Teacher Retirement Gap

For many educators, the retirement gap is the difference between what a pension is expected to provide and what retirement will realistically cost over a 20–30+ year retirement.

While teacher pensions can form a strong foundation, they are rarely designed to fully replace working income—especially when healthcare, survivor needs, and inflation are factored in.

Common contributors to the teacher retirement gap include:

Pension replacement limits

Even well-funded pensions often replace only a portion of pre-retirement income, particularly for educators who retire earlier, have fewer years of service, or experienced salary plateaus.

Inflation and cost-of-living uncertainty

Some pension systems offer limited or inconsistent cost-of-living adjustments (COLAs), which can reduce purchasing power over time.

Survivor income reductions

Choosing a joint-and-survivor pension option may significantly reduce monthly income, creating a gap for either spouse—while choosing a single-life option can leave a surviving spouse vulnerable.

Longevity risk

Teachers are often healthier and live longer than average, increasing the risk that fixed pension income may not stretch far enough in later years.

Healthcare and transition-year costs

Retiring before Medicare eligibility or before certain benefits begin can create temporary but significant income and coverage gaps.

the Retirement Gap Solved

Identifying the retirement gap early allows educators to make informed decisions about supplemental savings, income structuring, and insurance-based strategies that can help align pension income with real-world retirement needs.

The goal is not to replace the pension—but to support it, creating a more predictable and confident retirement plan built around your lifestyle, family, and timing.

Our Process At BTO Financial Group

This process is designed specifically for educators navigating pension-based retirement systems and retirement timing decisions.

initial discovery call

TEACHER RETIREMENT SNAPSHOT REVIEW

RETIREMENT SYSTEM AND PENSION OVERVIEW

PROTECTION & INCOME GOAL DEFINITION

GAP AND RISK IDENTIFICATION

EDUCATION BASED OPTIONS REVIEW

CUSTOMIZED RETIREMENT STRATEGY

Implementation & Secure Client Portal Access

ongoing reviews and life updates

Looking for more information?

Frequently Asked Questions

We understand lorem ipsum dolor sit amet, consectetur adipisicing elit.

Question 1: Do teachers get Social Security?

It depends on the state and the retirement system. Some educators pay into Social Security; others do not. We encourage confirming details with your retirement system and payroll records.

Question 2: What’s the difference between a 403(b) and a 457(b)?

Both are common supplemental retirement plans for educators, but they can have different rules about access, separation from service, and employer structure. Specific details depend on the plan.

Question 3: Is my pension enough to retire comfortably?

Sometimes yes, sometimes no. The right answer depends on your desired lifestyle, healthcare costs, debt situation, and whether you need survivor protection.

Question 4: Do I still need life insurance if I have a pension?

Many teachers do—especially if they have a spouse, dependents, a mortgage, or want to protect survivor income outcomes.

Question 5: When should i start planning?

Ideally several years before retirement so you have options. But planning can still be valuable at any stage.

Still Have Questions?

We have the Answers!

Contact

19220 Space Center BLVD, Houston Texas 77058

Texas +1 346-584-2454

North Carolina +1 984-464-8511

Virginia +1 571-946-1553

Providing education-focused guidance to help individuals and families make informed insurance and retirement planning decisions.

Our Social Media Sites will be live in Feb 2026

Business Hours

Mon - Sat : 9AM - 4PM

Sunday: 9AM - 4PM

© BTO Financial Group. 2026. All Rights Reserved.