All Services

Our Team

All Services

Family Insurance Guidance | BTO Financial Group

Protecting a family isn’t only about having “a policy.” It’s about creating a plan that helps your household stay financially stable if life throws a curveball—an unexpected death, illness, or loss of income.

Protecting a family isn’t only about having “a policy.” It’s about creating a plan that helps your household stay financially stable if life throws a curveball—an unexpected death, illness, or loss of income.

At BTO Financial Group, we take an education-first approach to family insurance planning. That means we’ll help you understand your options, compare strategies, and choose coverage aligned with your family’s needs—without pressure and without jargon.

Why Choose an Education-First Approach?

We emphasize education, clarity, and transparency to help individuals and families better understand insurance-based retirement planning strategies and make informed decisions.

01.

Education Comes First

We prioritize education and understanding, taking the time to explain insurance-based retirement planning options clearly—so you can make decisions that feel informed and comfortable.

02.

Transparent Planning Process

Our approach is built on clarity and transparency. We walk through available options, explain how different strategies work, and answer questions without pressure or obligation.

03.

Professional

Guidance

As a licensed insurance professional, we provide guidance focused on insurance-based retirement planning strategies designed to support long-term planning goals.

What “Family Insurance” Usually Means

When most people say “family insurance,” they’re typically talking about life insurance and related protection planning designed to support the people who depend on you financially.

01.

Replacing lost income so your family can keep paying bills

02.

Paying off major debts (mortgage, car loans, credit cards)

03.

Funding childcare and day-to-day living expenses

04.

Covering final expenses and medical bills

05.

Creating stability for long-term planning (education, legacy, and future goals)

06.

Providing liquidity at the right time so survivors aren’t forced to sell assets, drain savings, or make rushed financial decisions during a difficult period

What “Family Insurance” Usually Means

When most people say “family insurance,” they’re typically talking about life insurance and related protection planning designed to support the people who depend on you financially.

01.

Replacing lost income so your family can keep paying bills

02.

Paying off major debts (mortgage, car loans, credit cards)

03.

Funding childcare and day-to-day living expenses

04.

Covering final expenses and medical bills

05.

Creating stability for long-term planning (education, legacy, and future goals)

06.

Providing liquidity at the right time so survivors aren’t forced to sell assets, drain savings, or make rushed financial decisions during a difficult period

Clarity Makes Retirement Planning Simpler

Through an education-first approach, we help individuals and families better understand insurance-based retirement planning strategies and navigate important decisions with clarity. Our focus is on transparency, understanding options, and thoughtful long-term planning.

Clarity Makes Retirement Planning Simpler

Through an education-first approach, we help individuals and families better understand insurance-based retirement planning strategies and navigate important decisions with clarity. Our focus is on transparency, understanding options, and thoughtful long-term planning.

Who Family Insurance Planning Helps the Most

Family insurance is especially relevant if you are:

- Newly married or recently partnered

- A new parent (or growing your family)

- A single parent

- A homeowner with a mortgage

- Supporting aging parents or family members

- The primary income earner—or the primary caregiver

And yes—stay-at-home parents and non-working spouses often need coverage too. If something happened, the financial impact of replacing childcare, transportation, and household management can be significant.

How Much Life Insurance Do Families Usually Need?

There’s no one-size-fits-all number, but there is a smart way to estimate.

A practical needs-based review often looks at:

01.

Income Replacement

How many years of income would your family need?

02.

Debt Payoff

Mortgage, personal loans, credit cards

03.

Child Related Costs

Childcare, schooling, college goals

04.

Final Expenses

Funeral costs and potential medical bills

05.

Emergency Buffer

A cushion for unexpected expenses

A common mistake is choosing a number that “sounds reasonable” instead of matching coverage to actual needs. Education-first planning helps you connect the dots.

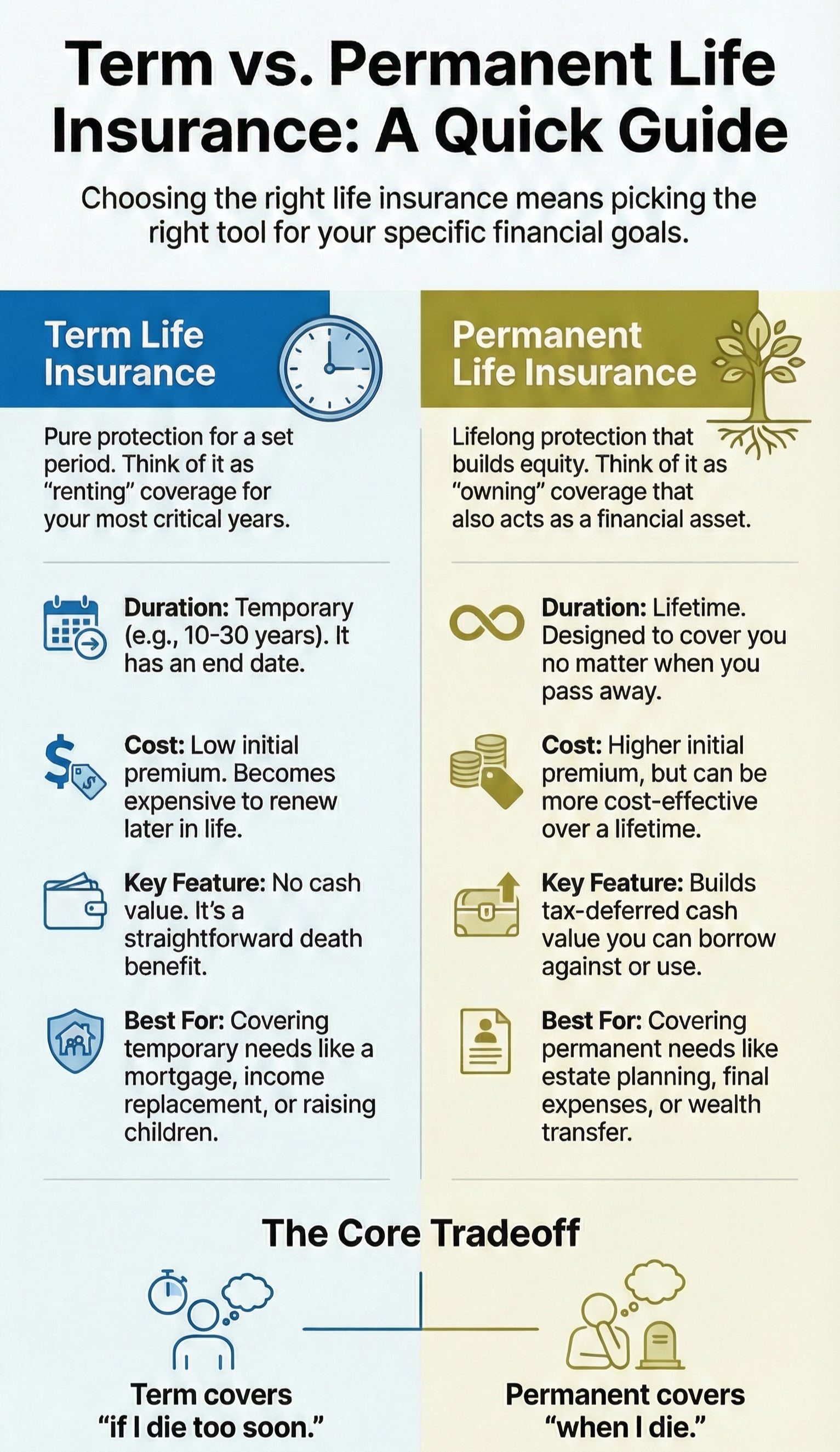

Term vs Permanent Life Insurance (In Simple Terms)

Term life is often used to cover high-need years (raising kids, paying a mortgage). It’s typically designed for a set period of time (like ten, twenty, or thirty years).

Often used for: income replacement, mortgage protection, young families on a budget.

Permanent coverage is designed to last longer (as long as the policy is maintained). Some types may build cash value, and some strategies are used for lifetime protection and legacy planning. These include WHOLE LIFE, UNIVERSAL LIFE and INDEXED UNIVERSAL LIFE Insurance.

Often used for: lifetime coverage needs, final expense planning, long-term family goals, legacy strategies.

The right mix depends on your goals, budget, health, and how long your family depends on your income.

Key Decisions Families Should Understand

When building a family insurance plan, the “details” are not small details. Education matters most in areas like:

01.

Policy Ownership - Who Owns the Policy and Why it Matters

The policy owner is the legal controller of the life insurance contract. This person (or entity) has authority to make changes.

What the owner can do:

Change beneficiaries

Adjust coverage or riders (subject to policy terms)

Transfer ownership

Cancel the policy

Access cash value (if applicable)

Why it matters:

Control ≠ Insured: The insured (the life being covered) is not always the owner. For example, a business may own a policy on a key employee, or parents may own a policy on a child.

Estate and tax implications: Ownership affects whether proceeds may be included in an estate, which can have tax consequences.

Divorce or business disputes: If ownership isn’t clearly aligned with intent, disputes can arise—even if beneficiaries seem correct.

Best practice:

Ownership should align with who needs control to fulfill the policy's purpose (family protection, business continuity, estate planning). Review ownership after major life events.

02.

Beneficiaries - Keeping them Accurate and Updated

Types:

Primary beneficiaries: First in line to receive proceeds

Contingent (secondary) beneficiaries: Receive proceeds if primary beneficiaries are deceased or ineligible

Why accuracy matters:

Life changes override intent: Marriage, divorce, births, deaths, and estrangement can quickly make beneficiary designations outdated.

Beneficiary designations usually override wills: Even if a will says otherwise, insurers pay based on the policy form.

Minor beneficiaries: Naming minors directly can delay payouts and require court involvement unless a trust or guardian is specified.

Best practice:

Review beneficiaries at least every 2–3 years and immediately after major life events. Use full legal names and clarify percentages.

03.

Coverage Length - Matching the Term to Years of Highest Risk

Coverage length (term) is how long the policy stays in force—commonly 10, 20, or 30 years for term insurance.

Why timing matters:

The goal is to cover financial vulnerability periods, such as:

Years with dependent children

Mortgage or rent obligations

Income replacement during peak earning years

Business debt or partner obligations

Too short = coverage may expire before risks end

Too long = unnecessary premium costs for risks that no longer exist

Best practice:

Map coverage length to your longest financial dependency, not your age alone. Many families ladder multiple terms (e.g., 20-year + 10-year) to reduce cost while maintaining protection.

04.

Riders (Optional Features): Customizing Protection

Riders are add-ons that modify or enhance the base policy. Availability and cost vary by insurer and policy type.

Common riders and why they matter:

Accelerated Death Benefit: Access part of the death benefit early if diagnosed with a terminal illness—useful for medical or end-of-life costs.

Waiver of Premium: Premiums are waived if the insured becomes disabled, preserving coverage during income loss.

Child Rider: Provides coverage for children, often convertible later without medical underwriting.

Conversion Rider (term policies): Allows conversion to permanent insurance without new health exams—valuable if health declines.

Trade-offs:

Riders increase premiums

Some duplicate existing coverage (e.g., disability insurance)

Others provide flexibility that’s impossible to add later

Best practice:

Add riders that protect against risks you can’t self-insure and that would be difficult or expensive to replace later.on for unexpected expenses

Our Process At BTO Financial Group

This process is built for families seeking clarity, protection, and long-term insurance guidance at every life stage.

initial discovery call

family needs snapshot

coverage gap analysis

options and

education

customized coverage strategy

application and underwriting suport

policy placement and approval

secure client portal access

ongoing policy reviews and life updates

Looking for more information?

Frequently Asked Questions

Some FAQ's are included below but we encourage you to request a slot on one of our Licensed Agent's Calendars to ensure you obtain the most accurate, thorough and up to date response.

Question 1: Is term life insurance “better” than whole life insurance?

Neither is universally better. Term often fits temporary needs (kids, mortgage). Permanent coverage may fit lifetime needs and long-term strategies. The right choice depends on your goals and budget.

Question 2: Do both parents need life insurance?

In many households, yes. Even if one parent earns less (or is a stay-at-home parent), the financial impact of losing childcare and household support can be large.

Question 3: Can I get coverage if I have health issues?

Often, yes. Options vary based on health history, age, and the type of coverage. We can explain what’s realistic and help you compare paths. We work with more than 30 carriers and know specifically which ones approve for certain health conditions.

Question 4: How long does it take to get approved?

Timelines vary. Some policies can be faster than others depending on underwriting requirements. We have access to instant approval policies.

Still Have Questions?

We have the Answers!

Contact

19220 Space Center BLVD, Houston Texas 77058

Texas +1 346-584-2454

North Carolina +1 984-464-8511

Virginia +1 571-946-1553

Providing education-focused guidance to help individuals and families make informed insurance and retirement planning decisions.

Our Social Media Sites will be live in Feb 2026

Business Hours

Mon - Sat : 9AM - 4PM

Sunday: 9AM - 4PM

© BTO Financial Group. 2026. All Rights Reserved.