All Services

Our Team

All Services

Mortgage Protection Insurance Options | BTO Financial Group

A mortgage is often the biggest financial commitment a family makes. Mortgage protection planning is about one simple question:

If something happened to you, could your family keep the home?

Mortgage Protection

BTO Financial Group provides guidance on insurance-based mortgage protection options designed to help cover outstanding mortgage obligations in the event of unexpected life events.

Why Choose an Education-First Approach?

We emphasize education, clarity, and transparency to help individuals and families better understand insurance-based retirement planning strategies and make informed decisions.

01.

Education Comes First

We prioritize education and understanding, taking the time to explain insurance-based retirement planning options clearly—so you can make decisions that feel informed and comfortable.

02.

Transparent Planning Process

Our approach is built on clarity and transparency. We walk through available options, explain how different strategies work, and answer questions without pressure or obligation.

03.

Professional

Guidance

As a licensed insurance professional, we provide guidance focused on insurance-based retirement planning strategies designed to support long-term planning goals.

Mortgage Protection vs PMI: Not the Same Thing

People commonly confuse these two:

01.

PMI (Private Mortgage Insurance)

Protects the lender if the borrower defaults.

01.

PMI (Private Mortgage Insurance)

Protects the lender if the borrower defaults.

02.

Mortgage Protection (Life Insurance Strategy

Mortgage protection (life insurance strategy) is designed to protect your family by providing money that can be used to cover the mortgage if the insured dies (and in some cases, depending on the product, other qualifying events).

PMI is a loan requirement.

Mortgage protection is a family protection strategy.

Clarity Makes Retirement Planning Simpler

Through an education-first approach, we help individuals and families better understand insurance-based retirement planning strategies and navigate important decisions with clarity. Our focus is on transparency, understanding options, and thoughtful long-term planning.

Clarity Makes Retirement Planning Simpler

Through an education-first approach, we help individuals and families better understand insurance-based retirement planning strategies and navigate important decisions with clarity. Our focus is on transparency, understanding options, and thoughtful long-term planning.

What Mortgage Protection Insurance Is Designed to Do

Mortgage protection is typically built around the idea that a life insurance benefit could be used to:

- Pay off the mortgage balance (fully or partially)

- Cover monthly payments for a period of time

- Protect surviving family members from needing to sell the home quickly

- Reduce financial stress during an already difficult time

Who Mortgage Protection Planning Is For?

Mortgage protection is commonly considered by:

01.

First-time Homebuyers

02.

Families with a new mortgage or refinance

03.

Households with one primary income earner

04.

Homeowners with limited savings reserves

05.

New Parents Who Want Stability for Their Children

06.

Anyone wanting to provide safety to their family

Common Mortgage Protection Approaches

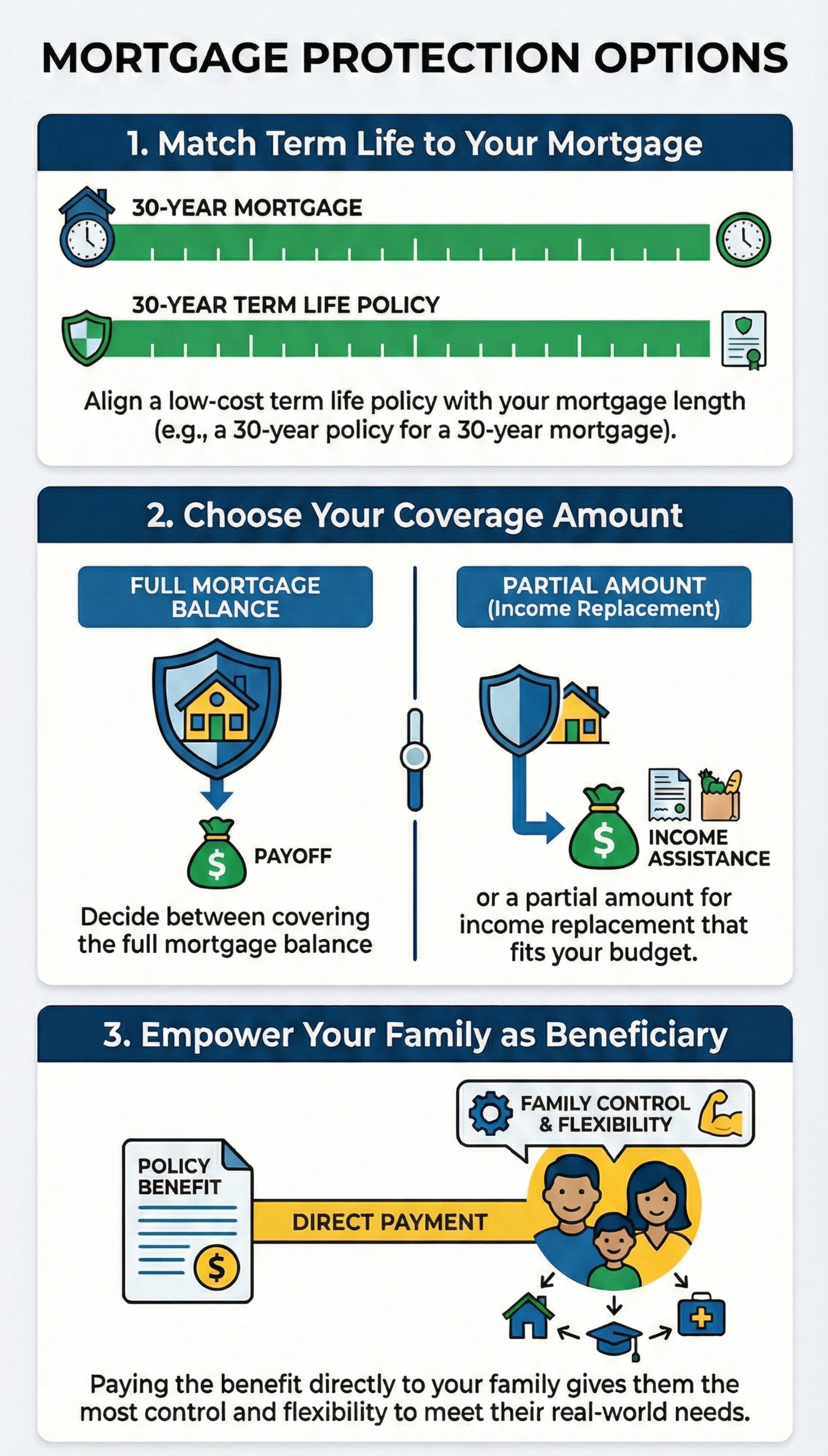

Term Life Insurance Matched to the Mortgage Term

Many homeowners choose a term length that aligns with the mortgage (for example, a thirty-year mortgage and a thirty-year term policy).

Why it’s used: straightforward, often cost-effective, flexible beneficiary choices.

Coverage Amount Options

Some plans aim to match the full mortgage balance. Others plan for a partial payoff plus income replacement.

What matters is choosing coverage that realistically fits your household budget and risk exposure.

Beneficiary Planning

Mortgage protection can be structured so the payout goes to a spouse/family member, who can then decide how to use the funds (pay off mortgage, cover payments, build emergency reserves).

Some people prefer pay-direct approaches, depending on the product and personal goals.

What Impacts Mortgage Protection Insurance Cost?

Pricing Typically Depends on:

01.

Age - At the Time You Apply for Coverage

Why it impacts cost:

Age is one of the strongest predictors of mortality risk. As age increases, the statistical likelihood of a claim rises, which directly increases premiums.

Key implications:

Rates typically increase every year, sometimes every birthday.

Locking in coverage earlier secures a lower rate for the entire term.

Waiting even 3–5 years can materially raise lifetime cost.

Bottom line:

You’re not paying for how old you feel—you’re priced on actuarial tables tied to your age at issue.

02.

Health History - Past and Current

Why it impacts cost:

Insurers price policies based on expected longevity. Chronic conditions, recent diagnoses, or unmanaged risks increase the probability of an early claim.

Key implications:

Controlled conditions (e.g., managed blood pressure) may still qualify for favorable rates.

Recent or severe diagnoses can increase premiums or limit options.

Full disclosure matters—misrepresentation can void claims.

Bottom line:

Better-documented and well-managed health usually means lower premiums and more carrier options.

03.

Tobacco Use - Recent and Current

Why it impacts cost:

Tobacco use significantly increases mortality risk, especially cardiovascular and cancer-related claims.

Key implications:

Tobacco users often pay 2–3× higher premiums.

Most insurers require 12–24 months nicotine-free to qualify for non-tobacco rates.

Occasional or social use can still trigger tobacco classification.

Bottom line:

Nicotine status is one of the fastest ways premiums can double—regardless of age.

04.

Coverage Amount

The death benefit paid out if the insured passes away—often aligned with the mortgage balance.

Why it impacts cost:

Higher coverage means higher potential payouts, increasing insurer liability.

Key implications:

Larger mortgages require higher coverage amounts.

Over-insuring increases cost without adding practical value.

Under-insuring can leave survivors exposed.

Bottom line:

Coverage should match the financial obligation you’re protecting—not exceed it unnecessarily.

05.

Policy Type - Term, Decreasing, Convertible

Why it impacts cost:

Different policy types expose insurers to different risk profiles.

Examples:

Level term: Fixed death benefit; higher cost but more flexible.

Decreasing balance policies: Benefit reduces as mortgage balance declines; usually lower premiums.

Convertible policies: Cost more due to added flexibility.

Bottom line:

Cheaper policies often offer less flexibility; more control and options usually come with higher premiums.

06.

Term Length - e.g. 15, 20, 30 Years

Why it impacts cost:

Longer terms mean the insurer is exposed to risk for more years, increasing the chance of a payout.

Key implications:

Shorter terms = lower premiums, but coverage may expire too soon.

Longer terms = higher premiums, but better protection during peak financial risk.

Matching the term to the mortgage duration is usually most cost-efficient.

Bottom line:

You’re paying not just for coverage—but for how long the insurer must stand behind it.

The best plan is one your family can keep consistently—not one that looks perfect on paper but collapses under the weight of monthly cost.

Our Process At BTO Financial Group

This process helps homeowners protect their mortgage, family, and home through structured insurance planning.

initial discovery call

mORTGAGE SNAPSHOT REVIEW

PROTECTION GOAL DEFINITION

POLICY options and

education

customized coverage strategy

application and underwriting suport

policy placement and approval

secure client portal access

ongoing policy reviews and life updates

Looking for more information?

Frequently Asked Questions

Some FAQ's are included below but we encourage you to request a slot on one of our Licensed Agent's Calendars to ensure you obtain the most accurate, thorough and up to date response.

Question 1: Is mortgage protection insurance required?

Usually no. PMI may be required by the lender, but mortgage protection is optional—chosen to help protect your household

Question 2: Can mortgage protection pay off my home entirely?

If structured that way, a life insurance benefit can potentially be used for payoff. The policy structure and benefit amount matter.

Question 3: Do I need mortgage protection if I already have life insurance?

Maybe. It depends on whether your current life insurance amount and term length adequately cover the mortgage plus other family needs.

Question 4: Can I qualify without a medical exam?

Some policies may not require an exam, depending on coverage type and underwriting guidelines.

Question 5: What happens if I refinance?

Refinancing can change the term and the balance—often a good time to review and adjust your coverage.

Still Have Questions?

We have the Answers!

Contact

19220 Space Center BLVD, Houston Texas 77058

Texas +1 346-584-2454

North Carolina +1 984-464-8511

Virginia +1 571-946-1553

Providing education-focused guidance to help individuals and families make informed insurance and retirement planning decisions.

Our Social Media Sites will be live in Feb 2026

Business Hours

Mon - Sat : 9AM - 4PM

Sunday: 9AM - 4PM

© BTO Financial Group. 2026. All Rights Reserved.